Considering a Credit Union Service Organization? The Basics You Need to Know

Credit union service organizations (CUSOs) have a history dating all the way back to the 1970s, when credit unions began exploring ways to collaborate and share resources to better serve its members. But, it wasn’t until 1987 when the National Credit Union Administration (NCUA) finally permitted the use of CUSOs. Historically, they were established to share services, resources, expertise and costs.

Over the years, CUSOs have been relied on more as revenue sources for credit unions seeking growth and sustainability. Today, there are over 1,000 registered CUSOs. Each plays an important part of credit union operations – leading the way to new frontiers, such as fintech and venture capital.

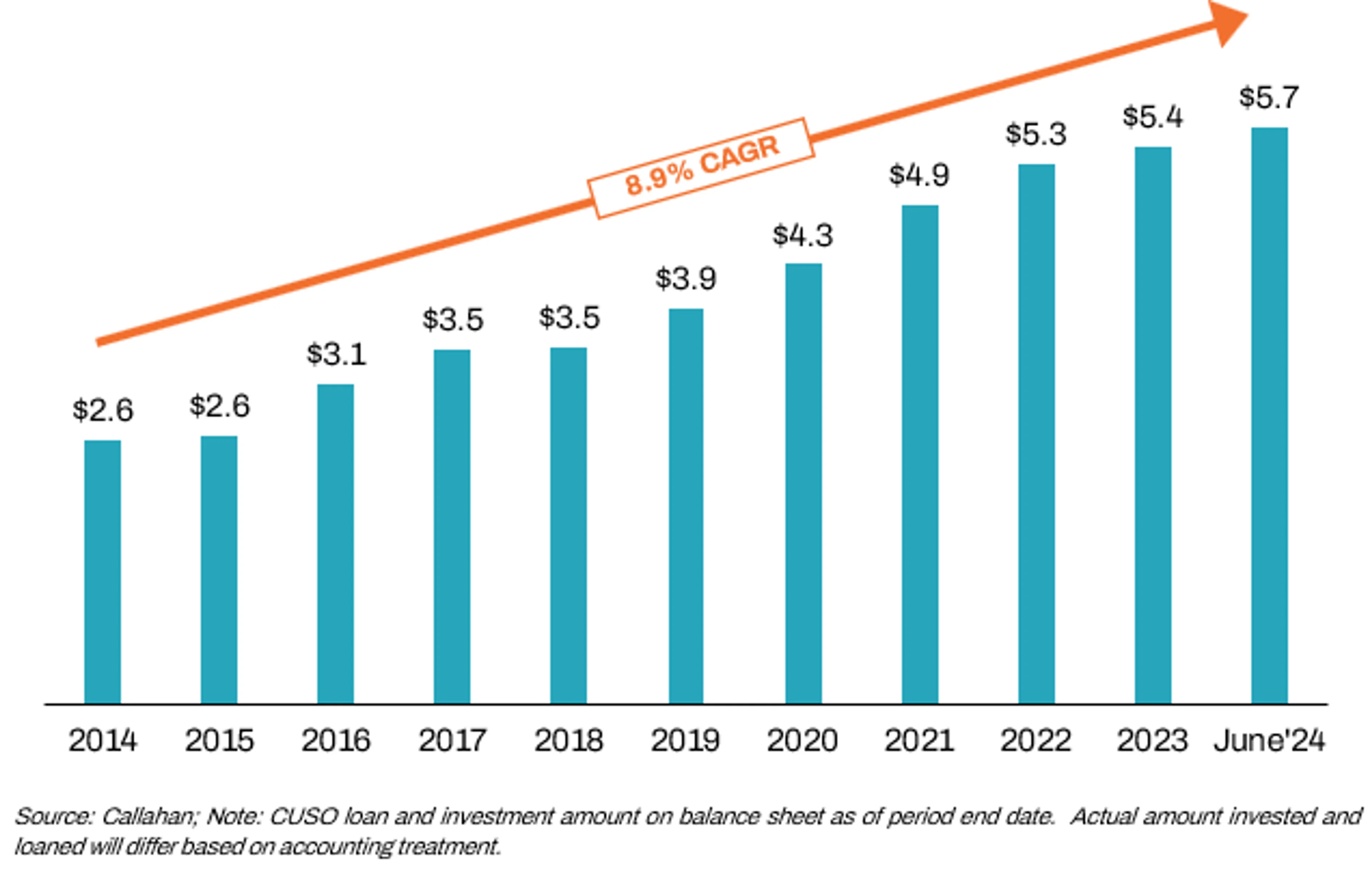

Depicted in the chart below, total credit union investment and loans to CUSOs has grown from $2.4 billion in 2014 to $5.7 billion in 2024, representing a combined annual growth rate (CAGR) of 8.9%.

Total Loans and Investments in CUSOs ($ in billions)

Permissible Activities

The NCUA monitors and limits the activities CUSOs can engage in to ensure they provide services closely related to the operations of credit unions and supports their mission and goals. Currently, the NCUA permits CUSOs to engage in the below activities:

- Checking and currency services

- Clerical, professional and management services

- Electronic transaction services

- Financial counseling services

- Fixed asset services

- Insurance brokerage or agency

- Leasing

- Loan support services

- Record retention, security and disaster recovery services

- Securities brokerage services

- Shared credit union branch operations

- Travel agency services

- Trust and trust-related services

- Real estate brokerage services

- Payroll processing services

- Loan origination

- Other

Entering the CUSO Space

Credit unions have three main options to enter the CUSO space:

- Form a new CUSO: Leverage internal expertise and moving functions or services off the credit union's balance sheet into the CUSO structure.

- Invest in an existing CUSO: Join other credit unions in an existing CUSO’s ownership and benefit from the services already provided.

- Acquire and convert: Acquire an established company and convert it into a CUSO structure assuming it meets all the CUSO eligibility regulatory requirements.

It is important to note, regulators do impose limits on how much a credit union can invest in CUSOs, depending on whether the credit union is a federal or state charter. Federally chartered credit unions can allocate up to 2% of their paid-in and unimpaired capital and surplus in CUSOs, with no more than 1% allocated to either loans or investments individually. While state-chartered credit unions vary and can be higher depending on the state’s regulatory framework.

Structure Considerations

CUSOs are typically structured as either C corporations or limited liability companies (LLCs), each with distinct tax implications. C corporations are subject to federal and state income taxes at the corporate level, and any distributed profits (dividends) are subject to tax again at the individual shareholder level, leading to double taxation. In contrast, LLCs offer a pass-through taxation model, where the profits and losses are passed directly to its owners and only subject to tax at the owner level. This structure provides limited liability to members while avoiding double taxation, making it a popular choice for credit unions looking for tax efficiency. As non-profit entities, credit unions generally do not pay taxes on income generated by its CUSOs structured as LLCs. However, if the IRS determines the income earned by the CUSO qualifies as unrelated business income (UBI), the credit union may be subject to Unrelated Business Income Tax (UBIT).

Ready to Consider Your CUSO Options?

Establishing or acquiring CUSOs takes knowing how they operate and ways to unlock their true value. Stay tuned as we explore unique ideas to unlock the potential value in upcoming articles.

If your credit union is ready to start exploring its options today, partner with our industry pros to help you navigate the complexities of investing in or starting a CUSO. We’ve got the perfect pairing of in-depth CUSO knowledge and technical expertise to position you for optimal success. Contact us today, we know the way.

David Milkes, CPA, CFA is the Principal of M&A and Strategic Services in Doeren Mayhew's Financial Institutions Group.